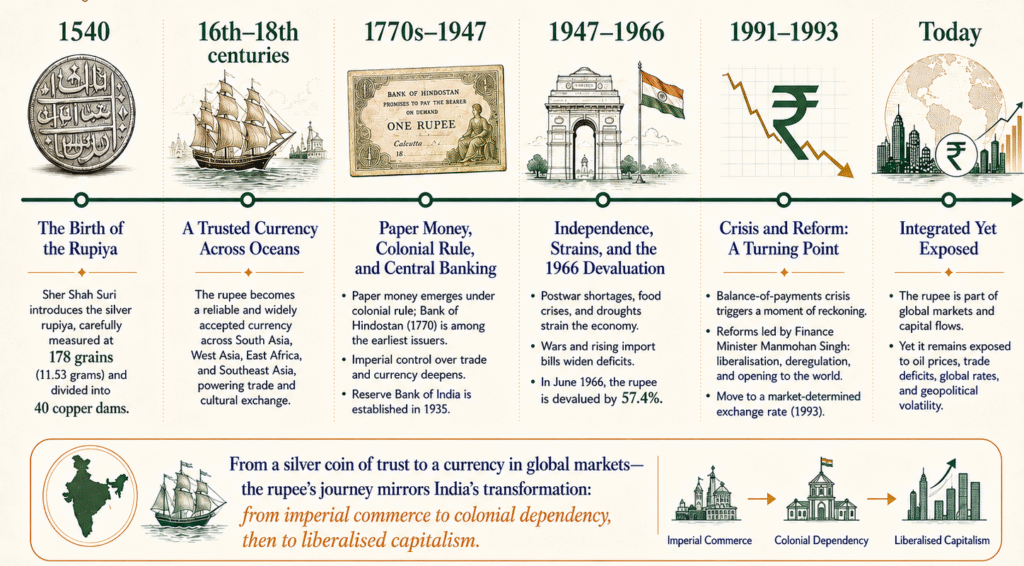

The story of the Indian rupee begins not in a modern central bank, but on the battlefields of sixteenth-century North India. In 1540, the Afghan ruler Sher Shah Suri, who established the short-lived Sur Empire after defeating the Mughals, introduced a silver coin called the rupiya. It was a carefully measured piece of silver weighing 178 grains (11.53 grams) and divided into 40 copper dams. The term is derived from the Sanskrit Rupyakam, meaning “silver coin.”

In a subcontinent fractured by kingdoms, local currencies, and competing authorities, the rupiya imposed consistency. Traders from Kabul to Bengal could trust its weight and silver content. Even after the Mughal Empire defeated Sher Shah’s successors, his monetary system survived. Empires changed. The rupee remained.

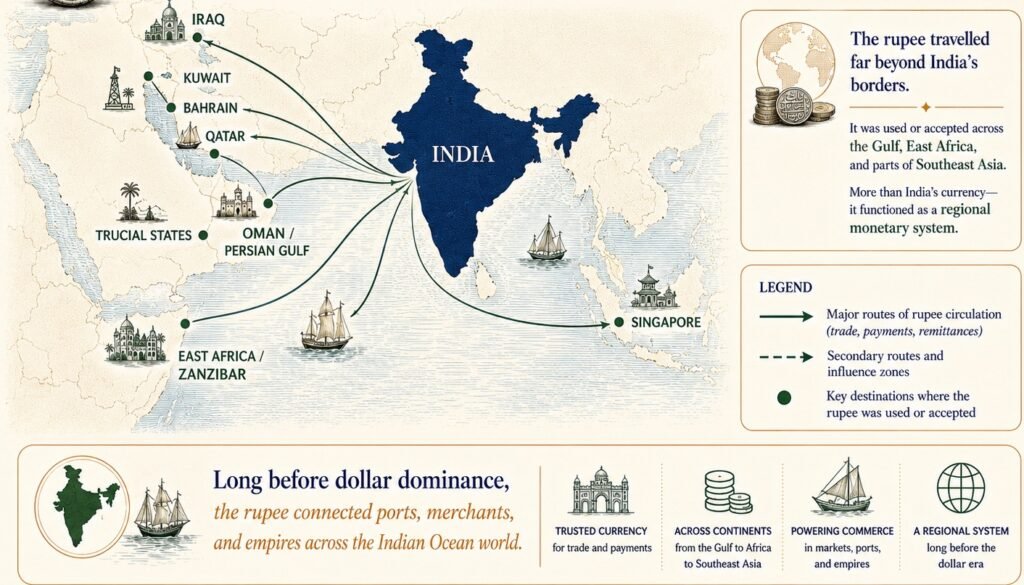

Long before the US dollar dominated global trade, the rupee circulated across the Indian Ocean world. In the Gulf, East Africa, and parts of the Arabian Peninsula, merchants accepted it as naturally as local currency. Oman, Bahrain, Kuwait, Qatar, and the Trucial States all used versions of the rupee. In East Africa, it functioned as legal tender under British colonial administration. Iraq used it officially until 1932. Even Italian Somaliland minted its own rupia to the same silver standard.

The rupee was not merely India’s currency. It was a regional monetary system.

Its reach reflected India’s commercial centrality in the Indian Ocean economy. Indian merchants financed trade routes stretching from Zanzibar to Singapore. Gujarati, Chettiyar, and Sindhi trading communities moved capital across ports where the rupee acted as a trusted medium of exchange. Stability, not military power, built its reputation.

The arrival of British rule changed the character of the rupee.

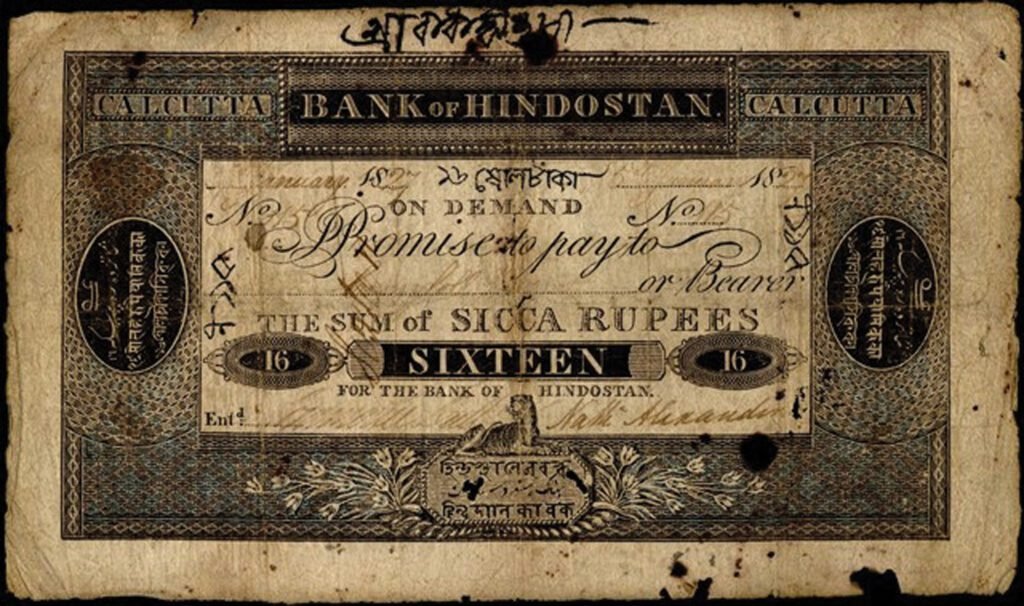

Paper currency entered India through private banks in the late eighteenth century. The Bank of Hindostan (1770–1832) was among the earliest institutions to issue notes. After the Revolt of 1857, the British Crown tightened control over Indian finance through the Paper Currency Act of 1861, centralising note issuance under imperial authority.

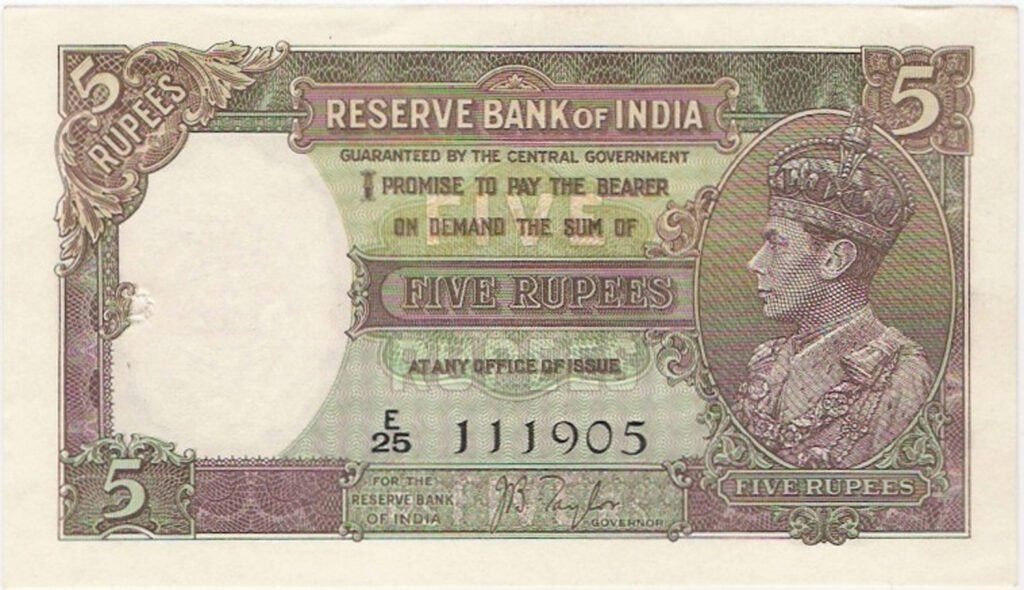

By the time the Reserve Bank of India was established in 1935, the rupee had become deeply embedded within Britain’s imperial financial structure. The RBI’s first note, a Rs. 5 bill bearing the portrait of George VI, entered circulation in 1938.

Even under colonial rule, the rupee retained extraordinary international standing. Its decline came rapidly after independence.

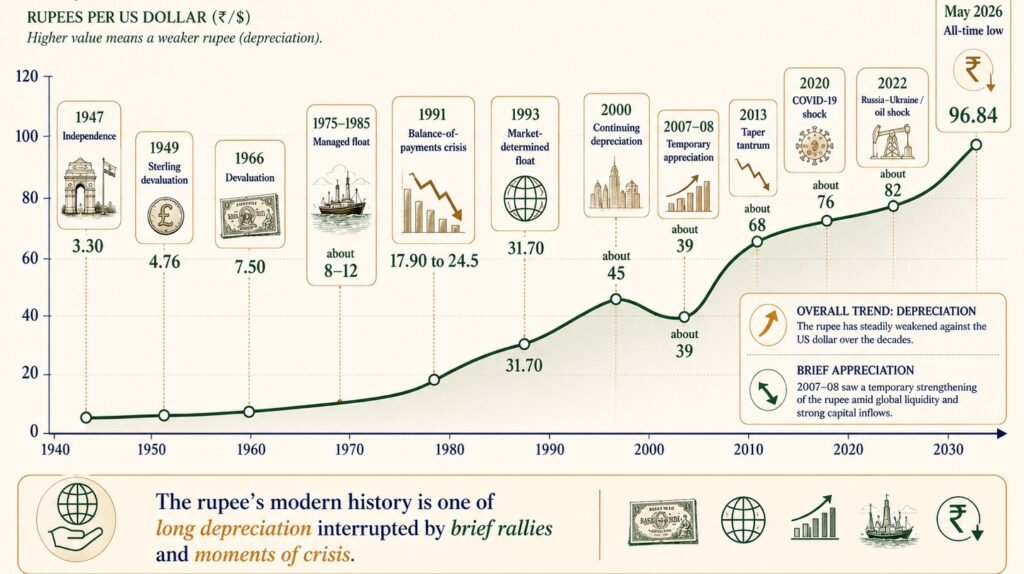

In 1947, one US dollar was worth roughly Rs. 3.30. Within two years, Britain’s postwar sterling devaluation pushed the rupee down to Rs. 4.76. But the real rupture came in the decades that followed.

India’s wars with China in 1962 and Pakistan in 1965, combined with severe drought and rising import pressures, strained the economy. On 6 June 1966, India devalued the rupee by 57.4%, taking the exchange rate to Rs. 7.50 per dollar.

The symbolism was devastating. A currency once trusted from Baghdad to Zanzibar had become vulnerable to crisis at home.

At the same time, India unintentionally dismantled the rupee’s overseas role. Gold smuggling through Gulf ports created pressure on India’s reserves, prompting the RBI to introduce a separate “Gulf Rupee” in 1959. But after the 1966 devaluation, Gulf states rapidly abandoned the currency, unwilling to anchor their economies to a unit that could suddenly lose value overnight.

A monetary sphere built over nearly two centuries collapsed within a decade.

The next turning point came in 1991.

India faced one of the gravest economic crises in its post-independence history. Foreign exchange reserves had fallen to levels sufficient for barely two weeks of imports. Gold had to be pledged abroad for emergency loans. Finance Minister Manmohan Singh responded with sweeping reforms: a sharp devaluation of the rupee, the dismantling of licensing controls, and eventually the transition to a market-determined exchange rate in 1993.

Liberalisation integrated India into global capital markets, but it also exposed the rupee to global volatility in ways never seen before.

Since then, the currency’s story has largely been one of managed decline interrupted by moments of panic. The 2013 “taper tantrum” pushed it to nearly Rs. 68 per dollar. The COVID-19 shock weakened it further to around Rs. 76. The Russia–Ukraine war and energy price spikes took it beyond Rs. 82.

As of May 2026, the RBI reference rate stood at Rs. 96.84 to the dollar, an all-time low. Rising oil prices, persistent trade deficits, and foreign investor outflows have intensified pressure on the currency. The RBI has intervened repeatedly through dollar sales and swap auctions, but interventions cannot fully offset structural weaknesses in a large energy-importing economy.

But the rupee’s story is not simply one of decline.

Its journey mirrors India’s own transformations: from medieval empire to colonial dependency, from post-independence austerity to liberalised capitalism.

Buried beneath the fluctuations of exchange markets lies a longer historical memory, of a currency that once connected ports, merchants, and empires across half the world.

Rupee vs. US Dollar: Depreciation & Appreciation Post-Independence

1-1024x768.jpg)